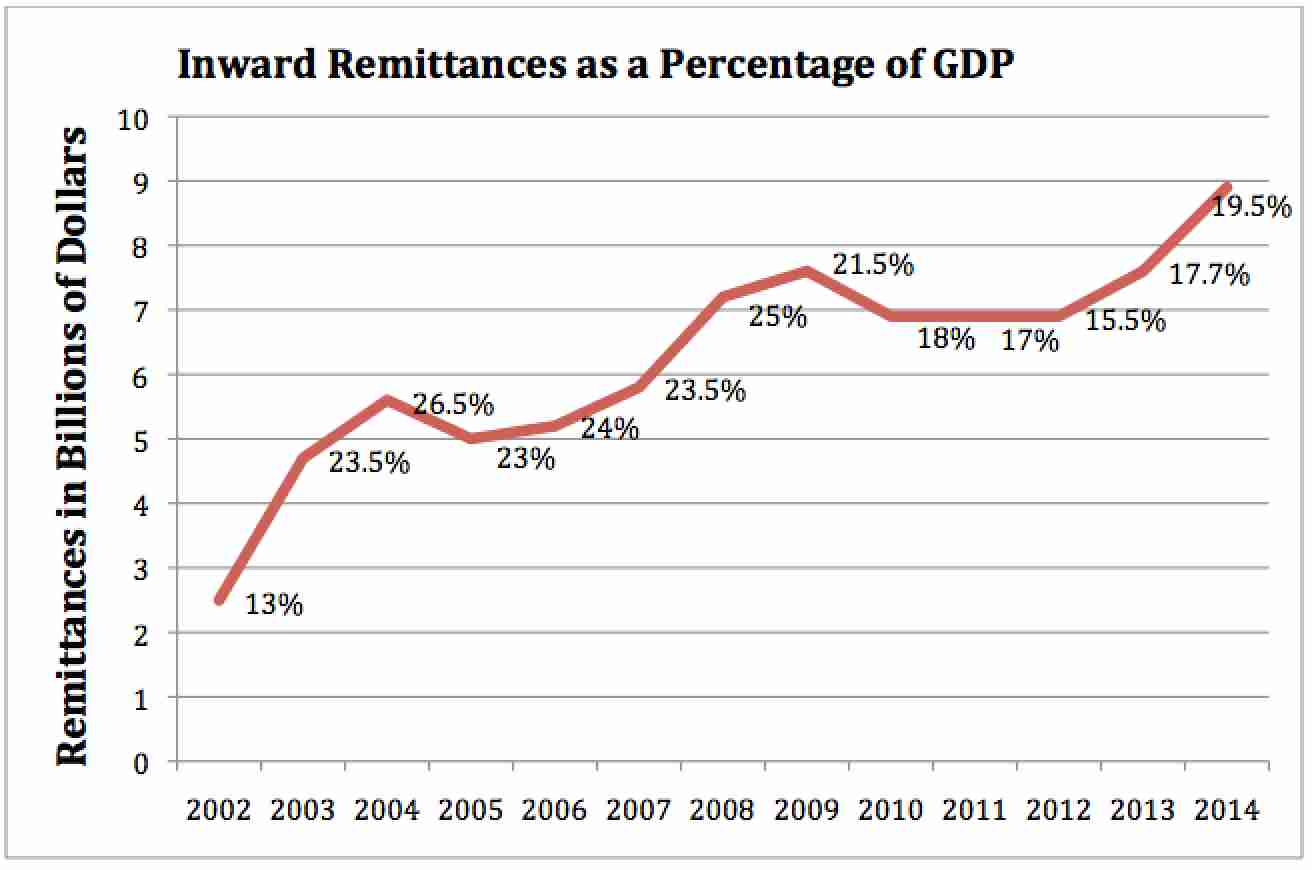

There are no official statistics on the numbers of Lebanese who have emigrated and are working abroad, nor on the immense sums of money they transfer to their home country. According to World Bank estimates, remittances comprised between fifteen and twenty percent of Lebanon’s gross domestic product over the past five years. More than half these remittances are earned in the Arab Gulf countries, where an average emigrant annually sends eight thousand one hundred US dollars back to Lebanon, while those in Africa and Europe/the Americas remit nine thousand dollars and four thousand three hundred dollars, respectively. These remittances are deposited in Lebanese banks, many of which have opened branches in the Gulf, West Africa and Europe to facilitate the accumulation of deposits.

Remittances not only sustain struggling Lebanese families in times of economic precarity but also support the state in this precarious time. Lebanon is mired in political polarization. One and a half million Syrian refugees are straining Lebanon’s already deteriorating infrastructure. Yet the highly indebted Lebanese state has issued 3.5 billion dollars in bonds in 2015. It was able to so successfully, despite the political and economic risks, because Lebanese banks are saturated with deposits, which total upwards of one hundred fifty billion dollars, or three times Lebanon’s GDP. This article traces the transnational political economy linking the remittances of the Lebanese diaspora to their investment in Lebanon’s burgeoning government debt.

[Data on remittances and GDP from the World Bank. Graph by the author.]

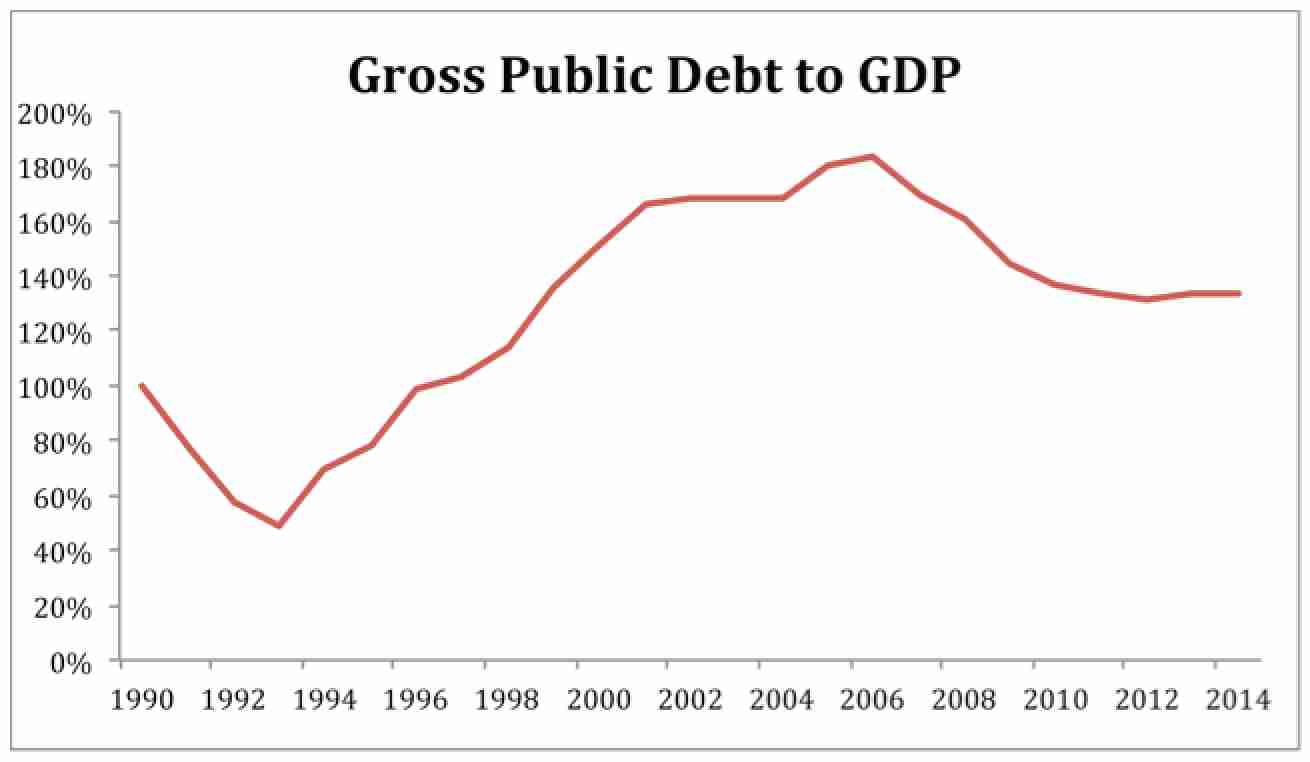

The trail begins in Riyadh, Dakar, or Paris; regardless of genesis, it often begins with the dollar, as the Lebanese lira has been pegged to the US dollar at a fixed rate of 1507.5 since 1998. A diaspora dollar is thus deposited in – for example – Bank Audi’s subsidiary in Doha, or BLOM Bank’s branch in Abu Dhabi, or Byblos Bank’s representative office in Lagos. The dollar can be withdrawn by family back home to pay for food, school fees, or heath care, or it could stay in a savings account earning interest. But the dollar does not idly accumulate interest in bank coffers. The banks invest more than half of their deposits in the sovereign debt, which is debt the Lebanese government has accumulated due to costly post-civil war reconstruction and chronic budget deficits. Lebanon is indebted by a conservative estimate of 132 percent of GDP, and rising, making it the third-most indebted country in the world (behind Japan and Greece).

Irrespective of where this diaspora dollar begins, it often ends up financing the debt of a government that is bankrupt in multiple senses, not simply financially. Yet Lebanon is not facing a financial crisis, and historically it has never defaulted on its debt. According to a former official at the Ministry of Finance whom I interviewed, the continuous growth in deposits, driven by remittances, is what “makes the economy continue. This is what makes Lebanon continue to refinance the debt of a government that in theory couldn’t finance itself.” Despite politicians better at lining their pockets than providing public services such as electricity, potable water, and garbage collection, bank deposits keep rising and Lebanon keeps sinking deeper into debt. The only thing that would break the system is if these deposits were to cease, but as economist Samir Makdisi told me in an interview, “You have this period since 1990 where you had wars, disruptions, instability, but nonetheless the rhythm of the outflow has not at any point imposed dangers that the system will break down.”

How was this system historically constructed? Why has this nexus of diaspora dollars, Lebanese banks, and sovereign debt not collapsed in the face of Lebanon’s perpetual political crises? How are these circulations of labor and capital to be understood—as part of a virtuous or a vicious circle? This is an especially important question in that capital flows are what keep the sovereign financially afloat, yet their persistence is made possible by exporting Lebanese citizens to work overseas.

History of Debt and Dollarization

Banking has long been at the heart of Lebanon’s laissez faire economic model. The liberalization of currency and capital markets in 1948 and the passing of the banking secrecy law of 1956 inaugurated Beirut’s role as a regional center of international finance. With the decline in political stability in neighboring Arab countries and the rise of oil income in the Gulf, foreign capital flowed into Beirut. From 1950 to 1974 the proportion of bank deposits to national income jumped from twenty percent to 122 percent – perhaps the highest in the world. With financial services the fastest-growing sector of the economy, bankers had become the most powerful economic actors before the outbreak of the civil war in 1975.

Remarkably, the first half of the civil war era coexisted with prosperity, and per capita income actually improved from one thousand four hundred dollars in 1974 to two thousand dollars in 1982. This is tied to an increase in oil revenues as well as the number of Lebanese emigrants in the Gulf, which rose from fifty thousand in 1970 to two hundred and ten thousand ten years on, or more than one third of the labor force. Their remittances rose from two hundred fifty million dollars in 1970 to 2.25 billion dollars in 1980, also more than one third of national income.

While the state’s authority withered under the weight of warring militias, the Central Bank remained effective. It kept the Lebanese lira stable at LL3 to the dollar and ensured there were no banking collapses during the war’s early years. Yet after the devastation of the 1982 Israeli invasion, and under the weight of military spending and public subsidies, the state’s budget could only be covered by borrowing from the banks. Lebanon’s public debt was negligible in 1975. Yet by the end of the war in 1990 it had risen to almost one hundred percent of GDP. The banks were burdened by mountains of debt but–in a prisoner’s dilemma–they had to keep rolling it over to prevent their own bankruptcy. As inflation accelerated in the late 1980s, the value of the lira collapsed, and people adopted the dollar as a medium of economic exchange.

Yet it was post-civil war reconstruction that devastated the Lebanese debt profile. The Rafiq al-Hariri administration wanted to restore Beirut’s prewar financial prowess with an eighteen-billion-dollar reconstruction program. They hoped that the widening deficit in government spending and mounting public debt would be contained by economic recovery. As Makdisi explained in an interview, initially few feared the debt, “the assumption that this was a temporary, short-term route to reconstruction . . . we will pile up debt, but we will pay that debt later on.” By 2002, however, public debt had risen to one hundred fifty percent of GDP, and the Paris II conference was convened to stave off a financial crisis. “The meeting was intended to simply save the Lebanese pound,” affirmed Makdisi in our interview. “The donors understood that if the pound had gone under then Hariri would have gone under, and that was not part of the political plan.”

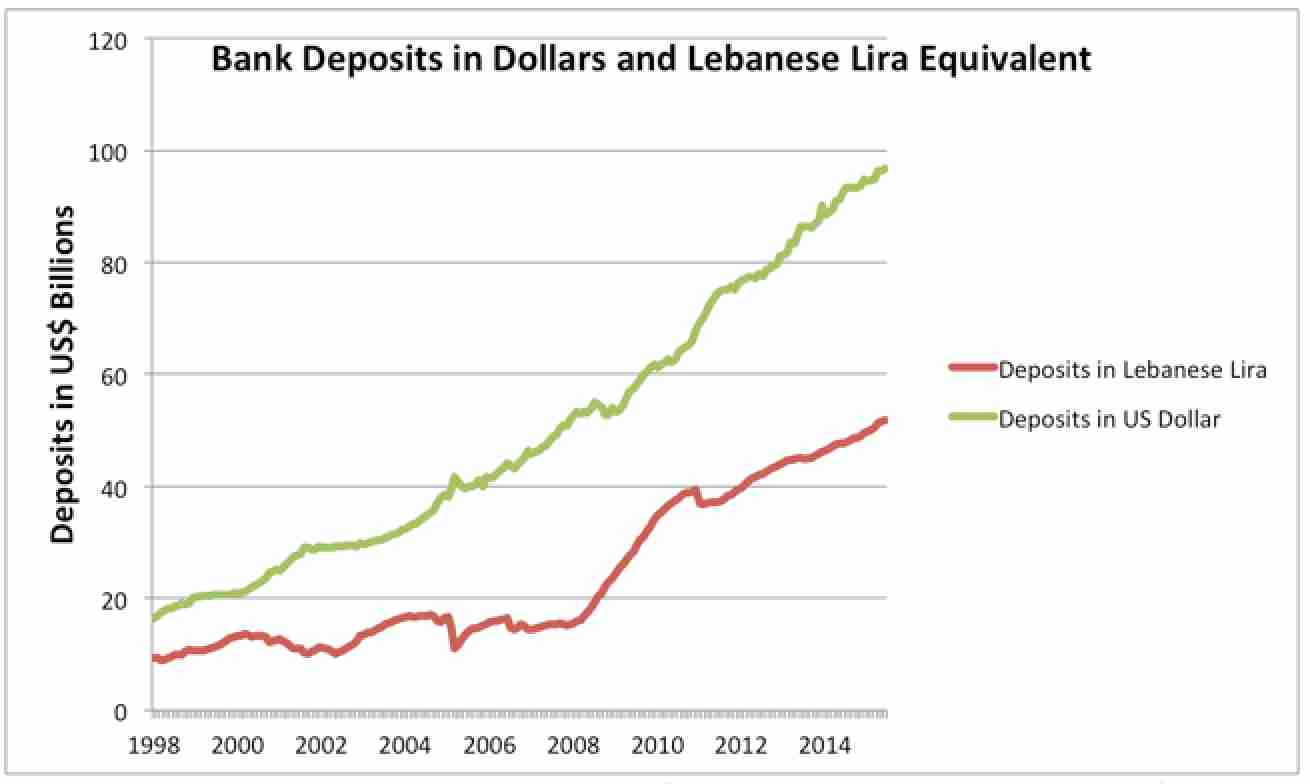

[Data from the Banque du Liban (www.bdl.lb). Graph by the author.]

Promises made at the Paris II conference to privatize, reduce spending, and raise taxes were broken, and Lebanon’s sovereign debt has since swelled. Debt peaked at one hundred eighty percent of GDP in 2006, but contracted to 134 percent of GDP in 2011 after a period of economic expansion. Lebanon’s debt is projected to grow due to the negative economic repercussions of the Syrian conflict. But surprisingly, deposits are still flowing into the banking sector. As dollarization was never reversed, the percentage of dollar-to-lira deposits tends to increase in times of uncertainty. Today, about sixty-five percent of deposits are in dollars. Economist Nisreen Salti has traced the impact of political instability on the economy and found that, rather than take their money out of Lebanon, depositors primarily deploy the tactic of switching their holdings from the lira to the dollar. Despite momentary outflows following the 2005 Hariri assassination and the 2006 war with Israel, deposits soon returned. Amid the global financial crisis, Lebanese banks were inundated with deposits because of confidence in the banks and the high interest rates they offered. Today, deposits continue to grow despite Lebanon’s political impasse and the impact of the Syrian civil war. Mounting debt, it seems, is not a deterrent for depositors, nor are the myriad of other political crises that Lebanon seems to perpetually face.

[Data from Banque du Liban (www.bdl.lb). Graph by the author. The ratio of dollar to Lebanese lira deposits

is taken as a confidence indicator in the Lebanese economy.]

Resiliency Explained

Lebanon has been without a president for over a year. Parliamentarians have twice extended their mandates without elections. One third of the country’s residents are refugees and most everyone faces daily electricity blackouts, water scarcity, and uncollected garbage. Yet, in the words of former Finance Minister Rayya el Hassan, “We are not a country in crisis as per the strict definition of a country in crisis as is known in the financial community.” This is because Lebanon faces few difficulties in financing its sovereign debt. How is this so? It is often explained by the concept of resiliency. Despite its myriad crises, Lebanon remains remarkably resilient. “Resilience underpins Lebanese debt,” is a headline from the Financial Times. Similarly, the credit rating agency Moody’s notes how Lebanese banks “have historically exhibited a remarkable resilience during periods of heightened political tension.” The World Bank affirms that Lebanon’s banks and their deposits “are resilient to shocks due to the diaspora’s familiarity with the country’s political and security volatilities.” However, the IMF writes in a recent economic assessment, “Lebanon’s renowned resilience is being severely tested.” This fear is echoed by the International Crisis Group, which argued that Lebanon’s resiliency has “become an excuse for a dysfunctionality and laissez-faire attitude by its political class that could ultimately prove the country’s undoing.”

I will conclude by more critically analyzing this resilience, but first I suggest three factors that make Lebanon thus: first, the nature of the Lebanese debt; second, the dollarization of the economy; third, the triad of the commercial banks, the Central Bank, and the sovereign–or as a former official at the Ministry of Finance described it to me, their monopolistic character.

In Argentina in 2001 and Greece in 2012, the two largest sovereign defaults in history, national debt was overwhelmingly owed to foreigners. However, more than eighty-five percent of Lebanon’s debt is held by Lebanese commercial banks and the Central Bank. A crisis of foreign bankers and traders pulling their money from Lebanon cannot happen because the overwhelming majority of investors are Lebanese. They are essentially locked into a circulatory financial system of bank deposits, high interest rates, and sovereign debt. The danger is of depositors withdrawing their savings from of the banks, but historically this has not happened. It did not happen when Lebanon came close to default before the Paris II conference in 2002, nor in the wake of Hariri’s assassination in 2005, nor amid the war with Israel in 2006, and not over the course of the Syrian crisis (although according to Bank Audi’s 2015 banking sector report, deposit growth slowed by twenty-five percent in 2014 compared to 2013). The source of much of these deposits is the diaspora, which the head of research at one of the largest banks described to me as “Lebanon’s sovereign wealth fund.” Their remittances are “a safety valve for the survival of the system,” in the words of an official at the Central Bank, and because their remittances are so diversified this decreases the risk. Much of the diaspora is based in Gulf Arab and African states. They expect to return to Lebanon, and thus they purchase homes in Lebanon and they continue to send their money back here. Lebanon’s banks facilitate these transactions by opening branches in a global network of countries where the diaspora are most present.

A second factor bolstering the stability of the sovereign debt is the strength of the currency peg. Following its devastating depreciation during the civil war, the Lebanese lira has been firmly pegged to the dollar for more than seventeen years. In economics there is a trilemma known as the “Impossible Trinity,” whereby it is impossible to have an independent monetary policy, a stable exchange rate, and the free movement of capital at the same time. To keep its capital markets open and maintain confidence in the currency, Lebanon has foregone an autonomous monetary policy, meaning that it must maintain high interest rates to attract deposits. Because there is confidence in the peg–that one dollar in deposits can always be withdrawn for one dollar in cash or exchanged for 1507.5 lira–Lebanon continues to attract depositors in both currencies because they believe that their deposits are secure. “The ultimate indicator of confidence in this country is the stability of the national currency,” affirmed Tom Jacobs, the country officer at the International Finance Corporation in our interview, “at the end of the day, resiliency comes down to the peg.” If the peg stumbles then deposits will likely fall too, making the banks struggle to purchase the sovereign debt, and thus bringing the financial system down with it.

Yet what most makes Lebanon financially resilient is the nexus of the commercial banks, the Central Bank, and the sovereign. Beyond preserving the stability of the exchange rate, the Central Bank’s other mission is to preserve the profitability of the banks. While one interviewee described to me this relationship benignly as a “tacit agreement to manage the system in a way that everybody makes money,” another maligned it as “a monopolistic, oligopolistic relationship to ensure the profitability of the banks.” The circulation of money between the banks and the sovereign–mediated by the Central Bank–has been essential in preventing a sovereign default or a currency crisis. It is the source of Lebanon’s resiliency.

Yet while the Central Bank has steered Lebanon through many storms, where most other countries would have faced financial collapse, it has not been without costs. There is an element of crony-capitalism in that many banks are owned by politicians in power. Economist Jad Chaaban has revealed the extent to which the politicians, as bank shareholders, are enriched by interest payments on the debt. Annually, around thirty-six percent of the government budget goes toward paying interest on the sovereign debt. Thus, former Prime Minister Saad Hariri, the largest shareholder in BankMed, earned 108 million dollars from interest payments on the sovereign debt from 2006 till today. Hariri is but one of many examples from across the political spectrum. Yet the banking–sovereign debt nexus is more complicated than simply a profit-making system for the politically connected. The Central Bank requires that the banks maintain high levels of reserves to buffer the economy in times of crisis. Their conservative management is one reason why deposits into Lebanese banks surged during the global financial crisis, and why deposits are still rising despite today’s political and economic risks. Most importantly, the Central Bank’s management–maintaining high interest rates to attract deposits and directing these deposits toward sovereign debt–is what keeps Lebanon from the brink of default.

Was Lebanon Not in Crisis before the Latest Crisis?

The diaspora dollar is at the center of a circulatory system that keeps Lebanon financially afloat. The flows of diaspora dollars, their deposit in the banking system, and investment in sovereign debt are part of a vicious and virtuous cycle. The virtuous part is that deposits make Lebanon more resilient to a financial crisis. Yet this resiliency is viciously responsible for exporting the Lebanese workforce. Because the banks are so invested in the sovereign and the sovereign is so steeped in debt, there is so little investment in public infrastructure or employment creation that many Lebanese look for work abroad. As a Central Bank official explained during our interview, “the vicious interpretation of it is that this political system, this economic structure, cannot capture the Lebanese who are young, who are educated, who in general have a lot of aspirations. Their leaving the country is what permits the system to survive.”

This requires a more critical look at the resiliency for which Lebanon has become so renowned. Is exporting an educated workforce the basis of resiliency? Is an economic system centered on rolling over ever-accumulating debt really financially sound? The question on the minds of many is, what will shock the system? What will cause deposits to dry up and thus prevent them from being translated into debt? But perhaps there is another, more profound, question: What are the consequences of a system centered on financing a bankrupt sovereign? Despite the corruption, dearth of democracy, and piling, putrid garbage, the Lebanese state can afford to go deeper and deeper into debt because that is where deposits are directed. Lebanon is not in the midst of a financial crisis, but it has long been mired in a governance crisis, one perpetuated by a political economy that prevents this very financial crisis from unfolding. The protests revealed that even garbage can be political. But in Lebanon–and in countries worldwide–the political is often overshadowed by the economic. My argument is that without understanding how this bankrupt political system is financed, it will be difficult to overturn it.

[The author would like to thank the participants at the Orient Institut Beirut’s colloquium for their helpful comments, as well as Lana Salman for first pointing out the concept of resilience.]