On 23 March 2020, Lebanon’s Ministry of Finance (MoF) announced it will “discontinue payment on all its outstanding foreign currency-denominated eurobonds.” On 27 March, the ministry made what is referred to as an investor presentation to the eurobond holders, explaining the government’s four-point economic recovery plan: commercial banks and central bank reform, fiscal reform, infrastructure and growth-enhancing investments, and the debt restructuring. Unfortunately, the presentation remained very vague on each of these points. The banking sector reform, we are told without further detail, would disentangle the links between the commercial banks and the central bank (Banque du Liban, BdL) and ensure the banking sector provides credit to the real economy. The fiscal reform involves cutting down on electricity subsidies and public sector pensions (the two usual suspects of austerity advocates), as well as improving tax collection and shifting the tax burden toward rentier income (how so?). The pro-growth agenda, finally, vaguely listed judicial reform, land reform, education, health, promotion of new dynamic industries, and gathering external support for high value-added infrastructure projects. Beyond that latter mention, there was no clear statement about foreign assistance. Noteworthy was the assurance that both the lira and dollar-denominated debt would be restructured, and the promise that the reforms and negotiations would be achieved by year end.

The first installment of this two-part article ended on the belated point made by the investor presentation, namely that the decision to restructure the debt “was driven by the necessity to safeguard BdL’s available foreign currency and allocate it exclusively to the payment of priority imports.” More generally, the article explained why there was no evading a default by outlining the nature of public debt in Lebanon in general and that of eurobonds in particular: both are key structural contributors to many of Lebanon’s economics crises—whether developmental, fiscal, or monetary—and have more to do with crony capitalism and state-banker networks than with genuine developmental strategies or market logics.

In short, in light of the debt’s crippling effect on the government budget discussed in the first part, any genuine solution to Lebanon’s economic crisis requires forgiving a sizeable portion of the outstanding public debt. Yet several analysts and commentators pushed against such policies in recent months. This second installment of the two-part article takes up some of these counterarguments as an entry point for further elucidating the nature of the crisis, the policies that produced it, and the effective remedies to it.

Those who have pushed forgiving a sizeable portion of the outstanding public debt have presented several concerns. Perhaps the three most circulated ones are:

- The measure will affect Lebanon’s credit worthiness, and thus limit future access to funds.

- The measure will kill Lebanon’s banking sector and hurt depositors.

- The measure would precipitate legal action and the potential loss of state assets.

As an alternative to slashing a portion of the outstanding principal, some of those raising the above concerns have suggested the following alternatives:

- Rescheduling the debt so as to postpone repayment and lower interest rates.

- Repaying externally-held debt but defaulting on the locally-held debt.

Let us address each of these two alternative proposals.

Alternative One: Rescheduling Rather than Restructuring

Lebanon’s current account deficit (the dollars that come into Lebanon less the dollars that leave Lebanon annually) is one of the largest in the world, and has precipitously increased from ten billion US dollars in 2015 to approximately sixteen billion US dollars in 2019. More importantly, Lebanon’s current account deficit is recurring. The drying up of foreign remittances and foreign aid combined with limited economic growth means that such a deficit can only be financed through new debt. However, as demonstrated in Part 1, public debt servicing already takes up a third of the annual state budget. New debt would only increase the debt servicing burden, which in turn would create even less of a margin in the annual state budget for policies in support of economic growth (e.g., infrastructural investment). In short, more debt would only perpetuate the problem. It is worth recalling that the rate of return to creditors on much of the debt is tremendously high. Thus even if the government demonstrated a willingness and capacity to invest more in the economy and to fund such investment through progressive taxation—both of which it has consistently refused to do in the last thirty years—there is little chance of reaching the growth rates and tax revenues necessary to service the debt toward full repayment.

In short, the current account deficit is unsustainable. Therefore, simply lowering interest rates and/or postponing repayment (even if interest free) will not work. All such measures would accomplish is to give the state a lifeline of a few years before debt servicing hits hard once again—thereby effectively prolonging the total period of debt and debt servicing.

Independent and internationally recognized analysts who have poured over the central bank’s opaque balance sheets have estimated that the debt will only become sustainable (i.e., actually repayable, given the size of the Lebanese economy) if the state slashes sixty to seventy percent of the outstanding debt. As the only sustainable solution, therefore, slashing the debt should have been done sooner rather than later, sparing whatever resources the public still has on its hands to relaunch the economy.

Alternative Two: Repaying Externally Held Debt While Defaulting on Locally Held Debt

Recall the nexus binding the central bank, local banks, and politicians in power, and the resultant aberrant profits the banking sector accumulated over the decades through the public debt. Some analysts consequently argue that the government could pressure local banks, who hold most of the public debt (including eurobonds), to forgive all or a significant amount of the principal. According to this argument, there would only remain the externally held debt, which is smaller and carries lower interest rates and is therefore more manageable.

However, distinguishing between externally-held and internally-held debt is a dubious basis for strategic action (even if a sound basis for understanding what has transpired in Lebanon over the last three decades). Local banks are constantly selling their eurobonds to foreign funds. If the decision is taken to repay the foreign creditors but not local ones, there is little doubt local banks will sell their share of the debt abroad overnight.

While the government could try to intervene and prevent such actions by the local banks—a difficult feat to imagine given the nexus of power between the two—legally speaking there is a growing grey area between what is locally held and what is held abroad. First, Lebanese banks have placed some of their eurobond holdings in fiduciary accounts abroad, that is, deposit accounts in which the funds are owned by one party but managed by another. When these funds collect an annual coupon payment or eurobond maturities, it is in fact unclear if they are doing so for those eurobonds they own or those they manage (i.e., owned by the local banks). Second, many local banks have entered into swaps and reverse-swaps with external funds. Therein, a local bank sells the bond to a foreign fund for its market value (e.g., thirty cents to the dollar) and then once the government repays the externally-held debt to the foreign fund, the local bank returns the market value to the external fund in exchange for the face-value repayment. The foreign funds charge the local bank a fee for the set of transactions. Moreover, the local banks might ask the foreign funds to send the principal repayment to the local bank’s accounts abroad—thereby evading the potential freezing of their assets (a regular administrative procedure in the case of bankruptcy) or other limits the state may impose on the movement of those funds. It is therefore quite likely that the strategy of exclusively defaulting on locally held debt would backfire.

Both alternatives to a fundamental debt restructuring are grounded in several concerns. Let us address each of these.

Concern One: Creditworthiness (and the Financial Engineering Scheme)

Creditworthiness reflects an entity's ability to pay back debt, or the likelihood the entity will repay a loan by meeting its financial obligations. The measure is determined by character (defined as honesty and reliability in repayment as evidenced by the entity’s credit history), capital (valuable assets with which to repay debt if income is unavailable), and capacity (ability to repay the debt given future income projections). Accordingly, Lebanon has not been credit-worthy at least since 2015, mostly as a function of the size of its outstanding dollar-denominated debt (i.e., low capital) combined with its persistent current account deficit (i.e., low capacity). In fact, since 2015 even the local banks were no longer willing to invest in eurobonds, as they saw that the dollar debt was becoming unsustainable. This would have been a good point in time to sound the alarm on state finances. Instead, the central bank governor Riad Salameh offered the local banks high interest rates in exchange for placing their dollars with the central bank, which he then used to purchase almost all eurobond issues by the Lebanese state since then.[1]

This is the context in which to understand the “financial engineering” scheme of 2016. The scheme has been presented to the public as an operation that buffers the BdL’s foreign exchange reserves and commercial banks’ capital in local currency. Not incidentally, the details of the scheme have not been officially disclosed. From what can be gleaned in the media, however, it seems it has another, concealed purpose. In reality, as of 2016 the MoF’s eurobonds were no longer attracting buyers in the market (proving the earlier point about Lebanon having already lost its creditworthiness). When bonds issued by a certain entity do not find buyers, the bid is very low, the market price ends up very low, and the rate of return to investors (or implicit interest rate paid by the issuing entity) is so elevated as to sound the alarm on that entity’s finances. The BdL’s financial engineering scheme was a way to avoid that situation, enticing local banks to buy Lebanon’s eurobonds by attaching this market operation to another: an exorbitant monetary gain denominated in liras. Here is how:

Briefly put, the financial engineering scheme consists of a swap of eurobonds and lira-denominated treasury bonds between the MoF and the local banks, where the local banks buy the MoF’s eurobonds (thus handing in dollars) and the MoF buys the lira-denominated treasury bonds held by local banks (thus handing them liras). The critical point is that the local banks get to sell the lira-denominated treasury bonds at an aberrantly over-valued price—literally a bribe denominated in liras to get the banks to buy the eurobonds. This is a simplification of the scheme. In reality, the BdL stepped in as an intermediary between the MoF and the local banks, engaging in two separate swaps: one between the BdL and commercial banks; and another one between the BdL and the MoF. In the first swap, the BdL sold the banks the eurobonds it bought from the MoF in the second swap. In the second swap, the BdL sold the MoF the lira-denominated treasury bonds it bought from the local banks in the first swap. In this way, the local banks, who were unwilling to lend the state another dollar, effectively extended the loan: the dollars flowed from the local banks through the BdL to the MoF. On the lira side, the treasury bonds moved from the banks’ balance sheets to the BdL’s to the MoF’s, where they are considered redeemed. However, while the MoF bought the treasury bonds from the BdL at market value, the BdL bought the treasury bonds at an exorbitantly above-market price from the local banks. In this way, the lira-denominated “bribe” sits on the balance sheet of the BdL (which can create liras), and not on the balance sheet of the MoF (which is more open to public scrutiny).

Because the BdL bought the lira-denominated treasury bonds from the banks at a price much higher than the price at which it sold these bonds to the MoF, the BdL incurred a loss. But that loss is denominated in liras, which the bank can create. There is an inflationary risk to that, and inflation would for all practical purposes act as a flat tax across the local population, cutting into the purchasing power of incomes and savings. While inflation can be avoided if the money created is reabsorbed by the central bank, that requires monetary policies that tighten credit and raise interest rates, pulling the breaks on economic growth.

This is in fact what the central bank ended up doing in 2017, to mitigate the inflationary risks from the liras it created in the financial engineering scheme of 2016. The 2017 BdL Circular 503 limited the lira-denominated credit offered by any bank to twenty-five percent of that bank’s lira-denominated deposits, knowing that the actual credit-deposits ratio at the time the circular was issued was approximately thirty-seven percent. In other words, in order to comply with the circular, the banks did not only have to stop extending credit. They actually needed to either decrease the amount of their outstanding loans to the private sector (which meant foreclosing more swiftly on non-performing loans) or attract additional lira deposits. The latter led to a competition between local banks, raising interest rates on lira deposits to extraordinary levels. Note that interest rates on dollar deposits had already shot up as banks competed among each other for dollar deposits to participate in the financial engineering scheme, raising the interest rates offered to unprecedented levels, reaching some fourteen percent (compared to a near-zero return on dollar holdings elsewhere around the world). It should be underlined that the hike in interest rates earned by depositors’ feeds into the reference rate (BRR or Beirut Reference Rate), which determines interest rates paid by borrowers in the private sector on commercial, housing, consumption, and student loans, among others. A great many of these borrowers, whose interest resets periodically to match the reference rate, defaulted.

The financial engineering scheme thus resulted in a halting of economic activity and much social hardship, which could constitute another article on its own. Despite its general praise for BdL governor Salameh, the World Bank noted as early as 2016 that the financial engineering scheme presented an unquantified “disadvantage” to the macroeconomy, whereby “rent is transferred from the public to the banking sector.” It then added a small comment in passing about the graver consequences: “such interventions can exacerbate macro-financial risks.”

These are all consequences the BdL was surely aware of when it undertook its financial engineering scheme. What mattered to the BdL, however, was that the MoF obtained new dollar loans with which to pay off the maturing dollar-denominated debt. To avoid the market price of such dollar loans being very low and the MoF incurring an aberrant implied rate of interest (which would have sounded the alarm in the market), the BdL subsidized the banks’ purchase of the eurobonds with liras. It thus incurred part of the implied interest in liras, so to speak.

The political significance of this implicit interest rate was highlighted in discussions about debt restructuring in early 2019. At the time, opponents to a restructuring pointed to what they claimed was the relative stability in debt servicing costs since 2016. For instance, the president of the Lebanese Economic Association stated:

The fiscal deficit at the end of the third quarter of 2018 is more than twice that of 2017 for the same period. Two main factors contributed to its escalation: the 21 percent rise in personnel cost generated by the wage and salary increases adopted in the last quarter of the 2017 budget, and the 8 percent escalation in the debt service cost. The latter reflects both higher debt and higher interest rates […]. Real rates, however, at the current inflation rate are near zero.

Real interest rates are nominal interest rates less the inflation rate. The above statement claims that the increase in interest rates attached to the public debt were only due to an increase in inflation, and that might very well be true. It is worth asking, however, what would the real and nominal rates have been, had the BdL not subsidized banks’ purchase of previous eurobond issues with aberrant profit in liras? And to what degree would those rates have inflated the debt servicing figure in the public budget, had they appeared on it? The real purpose of the financial engineering scheme was to make statements such as the one above look plausible. Point 26 of the IMF staff’s Concluding Statement of the 2019 Article IV Mission states the following: “BdL should […] let the market determine yields on government debt.”

In short, any talk about protecting Lebanon’s creditworthiness is out of touch with reality. Potential creditors are well aware of the lack of creditworthiness of the Lebanese government. This is to say nothing of historical precedence, in which 111 countries that defaulted over the last thirty years later regained access to the global market to raise debt at an acceptable cost.

Concern Two: Repercussions for the Banking Sector and Depositors

It is certainly true that the default will “hurt” local banks, because the latter have invested most of their capital with the state—either directly or indirectly through the central bank. In fact, the twenty banks that were subject to the revoked asset freezing on 4 March 2020 were the banks whose exposure to the BdL and sovereign debt combined exceeded forty percent of equity as of year-end 2018. Of those, fifteen banks had an exposure that exceeded one-hundred percent of equity, and four banks had an exposure that exceeded two-hundred-forty percent of equity.[2] It is also true that the default will hurt depositors in the Lebanese banking sector, given some three-quarters of all deposits in the Lebanese banking sector are invested with the state—again, either directly or indirectly through the central bank. However, the fate of banks and depositors in the context of a default can be disaggregated and separately addressed.

Although banks had profited enough from the debt servicing to cover the principal of their loans to the state, those profits have been distributed as dividends, and so the banks themselves will lose much of their capital after a default. They will thus need new capital. This funding, called “recapitalization,” is typically paid to the bank in exchange for newly issued shares (the old ones having become worthless) which provide a return over the long-term. While it would be expensive to recapitalize all the banks in existence today, it should be noted that the banking sector is currently over-sized relative to the economy: we have the second-largest banking sector in the world as measured by the ratio of total bank assets to GDP.[3] Merging current banks together would make the recapitalization cheaper, and we can do with much fewer banks. The current banks have neglected lending to manufacturing and agriculture, and some of them solely invest in public debt, thereby contributing absolutely nothing to the productive economy: why should they be saved?

Estimates of the losses to be taken by dollar depositors in the Lebanese banking system have ranged between forty and eighty billion dollars, which roughly constitute thirty-five to eighty percent of the total deposit base (i.e., total deposits in the local banking sector). But how this loss is spread across the depositors is not a given, and is precisely where politics and policies matter again. By expressing the loss in deposits resulting from debt restructuring as a tax, a supposedly democratically elected and accountable state can then make a sovereign decision as to who bears it.

Let us first understand the structure of local bank deposits:

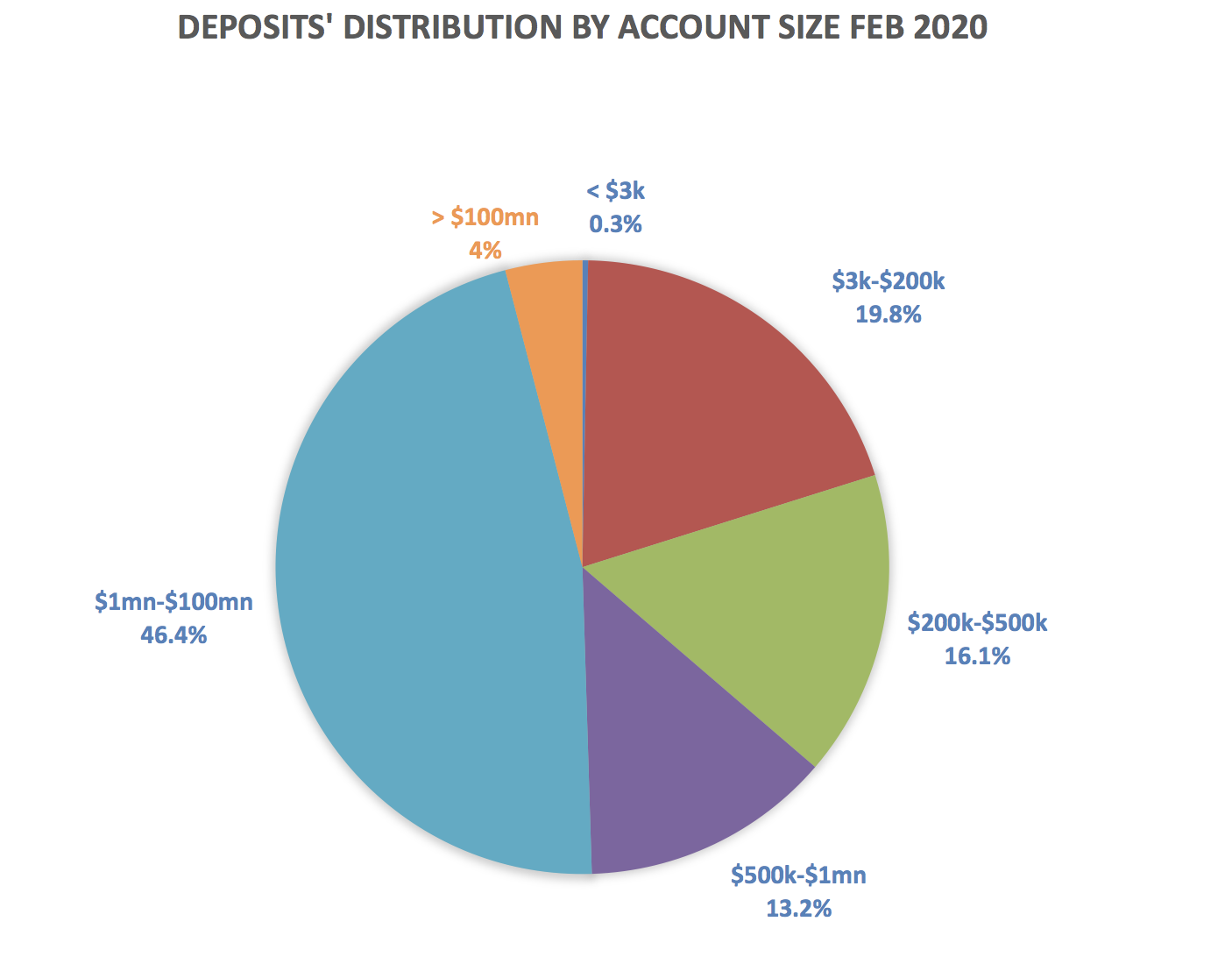

- Bank accounts holding over a million dollars each collectively add up to fifty-eight billion US dollars. There are approximately twenty thousand such accounts, probably held by some ten thousand individuals (who hold more than one account each).

- The accounts holding more than five hundred thousand dollars each add up to about seventy-three billion dollars. While these accounts constitute almost two-thirds of the total deposit base, they only represent two percent of all depositors (i.e., total number of people with accounts in the local banking sector.

- Bank accounts with over two hundred thousand dollars each add up to approximately ninety-two billion dollars. While these accounts represent eighty percent of the total deposit base, they only represent at most five percent of all depositors.

[Chart created by author utilizing data from 180 Daraje]

Given this level of concentration in dollar deposits, any loss resulting from a slashing of the principal of public debt (as advocated earlier) can be framed as a one-time progressive tax on large accounts, making them bear the brunt of the losses. This would spare anyone whose account holds less than two hundred thousand dollars, effectively separating the effect on the banking sector from the effect on most depositors. To clarify, this “tax” would not entail the transfer of actual dollars to the state. It would simply account for the irrecoverability of dollar deposits.

For this reasoning strategy to work, the government would need to act swiftly. In 2019, depositors with accounts holding more than one million dollars withdrew fifteen billion US dollars. The number of accounts holding more than one hundred million US dollars fell from thirty-six to twenty-three between January 2019 and March 2020.

Yet the thought of state seizure of individual private property (even through a necessary one-time progressive tax) goes against the dominant ideology undergirding the postwar Lebanese order. Even leading voices in the uprising temper their calls for such a measure by suggesting alternatives to an outright tax: forcible conversion to Lebanese pounds or bank equity rather than effective expropriation. Yet such alternatives would again lay the burden on the public. In the case of the first suggestion, this would occur through the inflationary effects of the necessary money creation. The second measure would compensate these millionaires with equity that would be the public’s if the state expressed the loss in deposits as a tax and participated itself in the recapitalization of the banking sector, purchasing bank shares with the funds freed up in the government budget as a result of the default on the public debt. In both scenarios, it is thus the broader public that bears the burden of debt restructuring rather than the large depositors.

Why should the broader public bear the burden? Progressive income taxes and wealth taxes which are now the norm around the world are based on the principle that those who have more should bear the larger part of any social cost—be it the cost of improving the road system or the cost of upending an unjust political economy. Moreover, someone who deposited one million dollars in a local bank ten years ago at twelve percent interest would today have that deposit worth 3.1 million US dollars. If we take away half of that total amount, the large depositor ends up with 1.55 million US dollars. In this instance, the account holder’s principle balance is intact, along with interest which breaks down to an average annual rate of 4.2 percent—a very decent rate of return on bank deposits by any standard. This piece of math illustrates that a one-time progressive tax on the largest deposit accounts who have been earning some of the highest rates of return (in the world) for this range of risk, and who have been enjoying one of the lowest tax rates (in the world) on this return, would merely bring their profits back in line with the global market.

On 3 April 2020, the BdL issued Circular 148, which was presented as a benevolent release of small depositors’ funds from the Lebanese banking system. The circular basically offers depositors with accounts below three thousand US dollars or five million liras to close their accounts in Lebanese banks within the next three months, after paying all their outstanding dues to the bank. According to the circular, the owners of dollar deposits can withdraw their balances in liras at the market rate. Those owners of lira deposits can withdraw their balances augmented by the ratio of the market exchange rate to the official exchange rate to compensate them for the loss of lira purchasing power (for instance, a depositor with three million liras would be able to withdraw four million liras, supposing the market rate is two thousand liras to the dollar). The circular specifies that each bank has to publicize the market rate at which it is trading each day. That figure may lie anywhere between 2,000 (the BdL-imposed ceiling on moneychangers’ bid for the dollar) or the actual market rate (currently at around 2,900). The extra liras paid to depositors will be provided by the central bank: pure money creation.

This move by the BdL and the current government, presented as an act of grace and appealing to the long-simmering resentments of the everyman, is hardly a course of action in everyman’s favor. The measure is in fact extremely inflationary. All these depositors closing their accounts will be holding their savings in liras. Since they will not be spending all their savings immediately, many will head straight to the money changers. The exchange rate will rise, and so will the price level. Sure, affected dollar depositors got hold of the lira equivalent to their dollars at the market exchange rate today, but the market exchange rate will be a multiple of that by the time they need to spend this money. And sure, affected lira depositors withdrew their lira savings augmented to adjust for inflation today, but inflation will be a multiple of that by the time they need to spend those savings.

The sum total of deposits that are subject to this circular across the entire banking sector is 344 million US dollars and 681 billion liras. That means when all is said and done, somewhere between 1,600 billion and 2,200 billion liras may be offered for sale at the moneychangers, depending on the market exchange rate and accounting for the required settling of debts. These amounts are significant relative to the money in circulation in the Lebanese economy, which was 19.5 billion liras in February 2020, up from 18.4 billion in January 2020. They are therefore very likely to sway the exchange rate at the moneychangers, hurting local consumers, the recipients of the amounts included. A real act of grace would have been to give the smaller depositors access to their dollars—and not the lira equivalent thereof. Despite claims to the contrary, this is possible: the dollar amounts involved are insignificant relative to the central bank reserves, the amounts owed to creditors, or the import bill. This would have truly benefited the account holders affected by this circular—more than 1.7 million (61.8 percent of all depositors in the Lebanese banking system)—and their increased consumption would have rippled through the economy.

Concern Three: The Legal Risk of Losing Assets Abroad

A public debt restructuring is most often a matter of negotiation with creditors. When the latter were unwilling to reach a compromise, however, states have defaulted on their public debt unilaterally–and this is when discussion of legal risk becomes pertinent. In Lebanon’s case, it is the foreign bondholders who pose a legal risk to the state. Up until mid-February 2020, however, Lebanon’s foreign creditors were clearly ready to negotiate, and the larger ones had made explicit statements to that effect. The eurobonds were offered for sale on the market at some thirty-five cents to the dollar. In other words, the market offer price was about a third of the face value. This reflects a clear expectation of default, and signals that creditors would be satisfied with a debt restructuring that offers them a third of the principal back, as opposed to a unilateral default which would entail a legal battle against the sovereign as well as a legal race against other creditors (because when one creditor gets repaid, there is less to go around for others—recall that states default because they are unable to repay the entire debt).

Critics of restructuring point to the fact that Lebanon’s eurobond terms do not include a provision commonly knowns as a collective action clause (CAC), and point to Argentina’s experience in 2001 as a precedent for what might happen in the absence of a CAC. A CAC is a standard bond feature that allows states to make changes to the terms of the contract of every issue of eurobonds with the consent of a specified percentage of bondholders that is greater than one half (at the rate of one vote per bond), and makes the changes binding on all bondholders, even those who oppose them. When Argentina announced a moratorium on the repayment of its public debt in 2001, its bonds lacked such a collective action clause. It consequently had to face off with over 1,500 individual lawsuits for more than fifteen years.

Up until 2014, the standard CACs applied to individual issues of eurobonds. For a government to restructure its debt, it had to negotiate with and obtain the consent of seventy-five percent of the holders of each issue of eurobonds. In 2014, following problems with both Greece and Argentina’s debt restructurings, the International Capital Markets Association published a standard form CAC with aggregation features—what came to be known as an enhanced CAC. In this new version of the clause, a single negotiation and vote has the power to bind all of a government’s many issues of eurobonds into a restructuring on the same terms. So rather than negotiating every issue separately and obtaining the consent of seventy-five percent of the holders of every outstanding issue, the post-2014 enhanced CAC allow a state to negotiate with all the bondholders across all issues at once, and obtain their consent on the new terms in a single vote. With the consent of seventy-five percent of the holders of all outstanding bonds, the state may restructure its entire debt. Needless to say, enhanced CACs make restructurings less work, less costly, and more immune to creditors who want to hold out and take the state to court.

Lebanon’s eurobonds include a CAC, but not an enhanced CAC—probably simply because the Eurobond contracts are automatically replicated from one issue to the next, without due legal diligence. Given Lebanon has twenty-nine eurobond issues outstanding, the state would have to make twenty-nine offers for a restructuring and obtain seventy-five percent of the vote every time, rather than make a single offer and obtain seventy-five percent of a single vote. This makes Lebanon in 2020 a fundamentally different case than Argentina in 2001. Also, it should be mentioned, while Lebanon is one of a few countries to have omitted the enhanced CAC from its eurobond contracts, it is actually one of only a few countries to have included the “regular” CAC before 2003. In any case, some of Lebanon’s outstanding bonds were issued before the enhanced CAC was even “invented” in 2014—and as long as some of its outstanding issues don’t include the enhanced CAC, a state cannot invoke that clause in the issues that include it.

For all those reasons, one could firmly argue that the legal risks from defaulting and restructuring were extremely inflated in public discourse. But that changed as of mid-February 2020, when Lebanon’s only aggressive creditor, Ashmore, came to own over 25.3 percent of the eurobond issue maturing in March 2020. This was made possible when local banks unloaded some of their eurobond holdings in an effort to evade potential government pressure to accommodate the public treasury, while at the same time getting paid abroad. It is worth noting that Ashmore is also invested in the sovereign debt of Argentina, Ecuador, and Venezuela, where it has been behind major lobbying efforts for repayment. The team behind these campaigns was the same one to have worked for famous vulture fund EMC, a “pioneer” in the business of buying up sovereign bonds and then suing defaulting governments.

This development imposes key new obstacles and constraints, but it does not mean that Lebanon does not stand a chance in a legal battle. It is still an open question whether lenders can cease the assets of the Lebanese state abroad if the latter defaults unilaterally. Most analysts argue that states have sovereign immunity against such seizures, but then this immunity may have been renounced contractually in the terms and conditions of some eurobond issues.[4] Assets held by the central bank might be immune because the defaulting entity is the treasury, specifically—unless the suing creditors can prove that these assets are held by the former on behalf of the latter. State assets that serve commercial purposes are more vulnerable; but then there is a legal requirement to prove that an asset has this characteristic. It is doubtful that such a characteristic applies to Lebanon’s gold reserve.

Critics of debt restructuring like to point out here that the Lebanese state lacks the expertise to take on such legal battles. Yet it is striking that whenever the Lebanese government resorts to multilateral institutions or multinational firms for consultation (e.g., the IMF or MCKenzy), the individual representing these parties is very often a Lebanese national. The expertise is not beyond the country’s reach if the government effectively decides to leverage it.

In conclusion, the alternatives to slashing sixty to seventy percent of the principal of the public debt outstanding are not viable solutions. Rescheduling (as opposed to restructuring) only postpones the problem and exacerbates the social costs; and the strategy of treating foreign and local bondholders differentially is practically impossible to implement. To the concerns raised about the impact of such a measure on Lebanon’s creditworthiness: the latter is lost already. The resulting losses to the banking sector and depositors can be controlled and distributed fairly by sovereign decision. Sure, there are significant legal risks, but these remain risks, and the loss of assets abroad is by no means as foregone as supposed.

The current economic model has clearly self-consumed. Yet the change should not only come out of necessity. Yes, Lebanon has to restructure its debt because it is out of dollars with which to repay its eurobonds. But this crisis should be seen and felt further as an opportunity for deep and revolutionary change. Facing up to the international creditors and the rentiers of this country, recognizing the role of the state, whether in securing these actors’ profits or in establishing a healthy redistribution, and building a productive economy that offers growth opportunities and lifts all its participants from precarity, are all actions that will carry this society into another dimension of global politics that cuts across the remote geopolitics of East and West—into the deeply human and personal global politics of the 99 percent, of gender equality, and of environmental activism.

[Click here to read Part 1]

[1] As of 2015, the BdL introduced certificates of deposits with longer maturities of fifteen, twenty, and thirty years—an excuse to raise the interest rates paid to lure banks to place their dollars with the BdL.

[2] Equity is the total of assets that remains to the owners of a business after the business’s liabilities have been covered. The ratios given in this paragraph were compiled by activists drawing on Bilanbanques.

[3] As per the governments’ presentation to bondholders on 27 March 2020, slide 14.

[4] The fine print on Lebanon’s eurobonds is still subject to debate. For instance, see here and here.